On 7 May 2026, the results from the third edition of the European Hydrogen Bank (EHB) were published. A total of €1.09 billion was allocated across nine projects with a combined electrolyser capacity of 1.1GW.

Over the first ten years of their lifespan, these projects will see the production of 1.3 million tonnes (Mt) of RFNBO and low-carbon electrolytic hydrogen and the reduction of around 9 Mt of greenhouse gas emissions.

After this successful round, and the many lessons learned and improvements made from the first two auctions, it is clear that the EHB is proving to be one of the most valuable funding tools for first mover projects in the hydrogen space.

The €3.3bn budget allocated to the Bank by the European Commission was divided into €800m for the first auction, €1.2bn for the second, and €1.3bn for this year’s edition. Notwithstanding the fact that not all this money has been or will be disbursed, it is time the European Commission renews the EHB. But the prospect of that is currently unclear and, with the freshly announced EU Industrial Decarbonisation Bank (IDB), there is a new and interesting angle to consider.

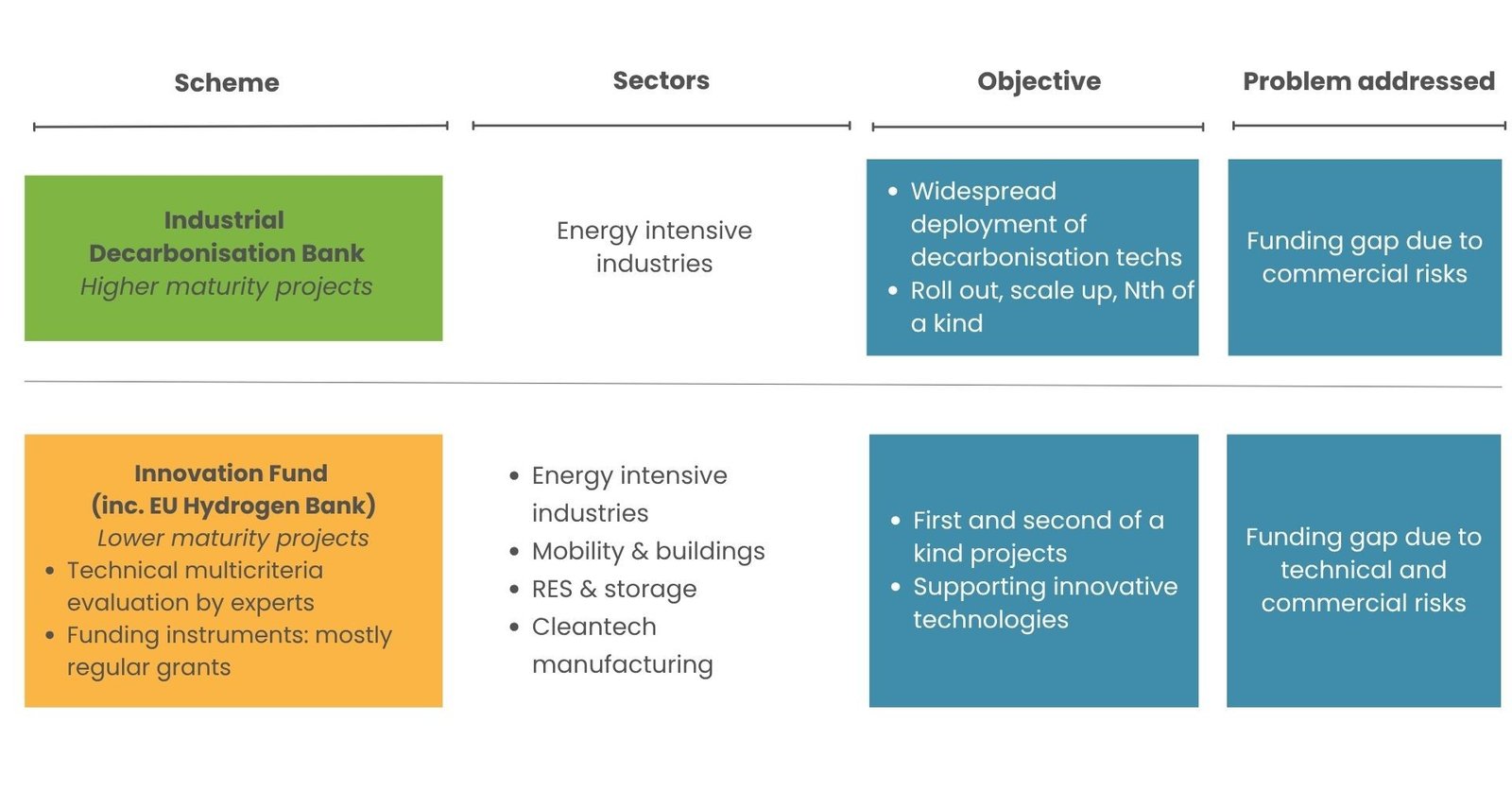

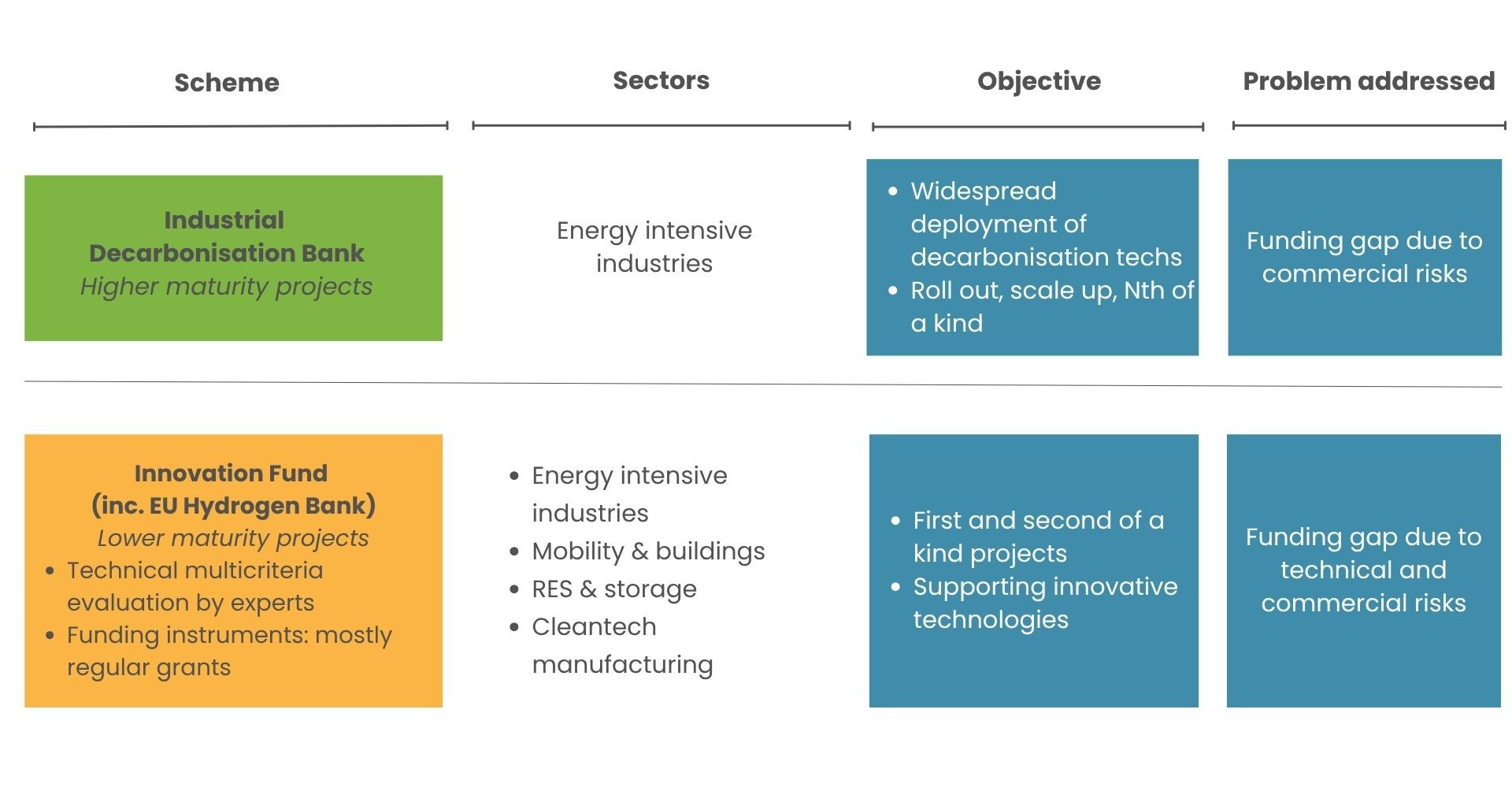

The Industrial Decarbonisation Bank

Figure 1: Scope of the Industrial Decarbonisation Bank, done by Hydrogen Europe based on a European Commission presentation.

While the exact structure and details will still need to be worked out, this is a very promising development. We understand that the IDB will focus on decarbonising energy intensive industries, so the new bank will be used to create industrial demand for decarbonisation technologies. For clean hydrogen and its derivatives, this is hugely promising as offtake risk is the biggest challenge for early-mover hydrogen projects: along with the EHB providing supply side support, a well-designed IDB would provide funding access both to hydrogen producers (EHB) and users (IDB).

Make it fit for hydrogen!

Hydrogen and its derivatives have an important role to play in Europe’s climate and competitiveness objectives, and we expect the IDB to crowd-in all decarbonisation technologies based on their potential contribution to our goals of net zero and energy resilience. This means avoiding the temptation to focus on low-hanging fruit and instead addressing the harder-to-abate sectors too, many of which will rely mainly on clean hydrogen.

To do so, the bank must look further than present-day cost efficiencies. Earlier stage technologies and sectors must be supported now so that they can play their part throughout this climate mission. Ensuring fair and broad competition across decarbonisation pathways must remain a guiding principle of the IDB. Therefore, the criteria for the planned auctions should reflect system-level costs and greenhouse gas reductions too.

Different mechanisms and funding instruments should be available to bidders depending on suitability and industry needs. Contracts-for-Difference (CfD) or Carbon -Contracts-for-Difference (CCfD) are both strong options to support demand, while embedding blended finance and other risk-sharing instruments would lend more support to de-risk offtake, while developing project finance structures and overall bankability.

Finally, we would urge that the Commission consider including aviation and maritime fuels in the IDB, as their production is an energy intensive process too.

European Hydrogen Bank (support to producers) must stay

The twin swords of the IDB and EHB would ensure effective funding support for clean hydrogen projects at a time when the sector is just beginning to deliver on its promise. For this to happen, the EHB must be renewed!

The original budget has not been fully allocated, and there could be hundreds of millions of euros left on the table. Longer-term the Bank should be continued in the following years with annual calls.

Despite some withdrawals during contractual negotiations, the growing success of the EHB is clear. We’re seeing projects from a wider geographical spread submit winning bids as the roll-out of the RED III legislation gathers pace and cross-border infrastructure projects are agreed upon (like between Denmark and Germany). The Auction-as-a-Service component has seen Member States almost match the EU contributions in additional funds to the EHB – including three times more during the 2nd auction.

There is of course room for fine tuning of the EHB, and Hydrogen Europe looks forward to contributing to that work.

For best results: support supply and demand

Finally, especially in emerging value chains – where supply and demand must scale simultaneously – better coherence, clear and pragmatic cumulation rules (including with State Aid frameworks) are needed to help close these financing gaps and ensure a strong scale-up.

So, to allow the IDB and EHB to work in tandem, we must ensure that hydrogen projects – which generally encompass multiple elements of the value chain – can benefit from both, overcoming possible current barriers linked to aid cumulation.

This is an excellent opportunity to scale Europe’s hydrogen and clean technology sectors right when we need them most. Let’s get it right.

Jorgo Chatzimarkakis is CEO of Hydrogen Europe