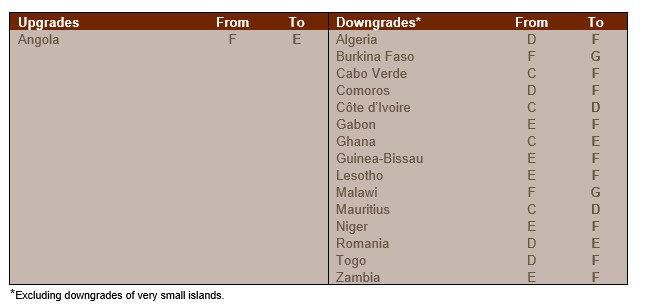

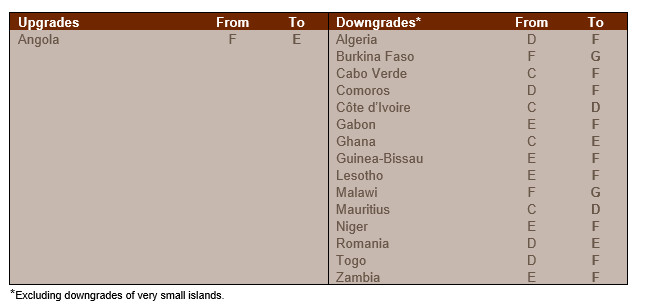

In the framework of its regular review of the business environment risk, Credendo has upgraded one country and downgraded eighteen countries. Although a fragile agreement between the US and Iran has been signed and has allowed the Strait of Hormuz to reopen, the impact of the Middle East conflict has led to many downgrades in Sub-Saharan Africa.

Business environment risk

- Angola upgraded from F/G to E/G

Angola’s business environment risk classification was upgraded from the second-highest category, F/G, to E/G. Economic performance is supported by a diversification investment drive in infrastructure, mining, agriculture and logistics. Inflation has fallen by more than half over the past two years, reaching 10.9% in May 2026. Angola is a net fuel importer that is capitalising on high international oil prices in the short term. Meanwhile, after a decade of falling output, oil production may finally stabilise thanks to renewed investor interest in the Angolan oil sector. Nevertheless, high debt-servicing needs in 2026 and 2027 will sustain pressure on liquidity. Foreign exchange availability is managed by the BNA (Banco Nacional de Angola), and the kwanza is kept broadly stable at around 917 AOA/USD under a managed float, with indications of some remaining misalignment. Overall, the management of the currency regime has been gradually improving.

- Sub-Saharan Africa: thirteen downgrades

The conflict in the Middle East has triggered a series of downgrades in Sub-Saharan Africa. Although the recent US-Iran agreement has led to a cautious improvement in the outlook, the restoration of disrupted supply chains and damaged Gulf infrastructure will be gradual. In addition, the ceasefire is highly fragile, with recent attacks illustrating the persistent risk of renewed escalation.

The Iran-US conflict has caused severe adverse spillovers for numerous African economies, especially net fuel importers. Elevated energy import costs and the risk of fuel shortages increase transport costs, fuel inflationary pressures and exacerbate currency vulnerabilities. At the same time, disruptions to fertiliser supply will constrain future agricultural production, leading to lower harvests and higher food prices, thereby heightening the risk of social unrest and political instability in the most vulnerable countries. Beyond these price effects, the conflict may also dampen external financial inflows. Lower foreign direct investment from Gulf States, combined with a potential decline in remittances, reduces an important source of external financing for several African economies. Ultimately, growth prospects for almost all Sub-Saharan African countries will be revised downwards for 2026, although some are more exposed than others and only a few could experience short-term benefits from higher global fuel prices, such as Nigeria and Angola. Vulnerabilities are expected to be compounded by extreme El Niño weather events, another upcoming shock likely to reinforce the impact on food security and inflation.

- Cabo Verde: The small and fully import-dependent island economy declared a state of emergency in March 2026 due to fuel shortages and soaring energy prices.

- Côte d’Ivoire: Higher fuel and fertiliser import costs are raising inflation, while high refined fuel subsidy costs are negatively impacting public finances and are likely to erode any gains from higher oil and gas export revenues.

- Gabon: The net oil exporter is experiencing severe fuel shortages due to its lack of refining capacity. Fuel prices have doubled and led to a national energy emergency in March 2026. High fuel subsidy costs have become an additional fiscal burden on already strained public finances.

- Malawi: One of the worst-affected countries in the region has experienced severe economic disruptions. The landlocked country’s strategic fuel reserves had already been exhausted before the Iran-US conflict erupted, due to chronic foreign exchange shortages. Widespread supply shortages have led to a doubling of fuel prices at the pump since the end of 2025, and depleted foreign exchange reserves have forced the central bank to sell its gold holdings to raise liquidity to finance fuel imports.

- Togo: High global fuel and fertiliser prices are increasing transport and food costs, pushing up inflation. Limited fiscal space is being further strained by fuel subsidies, while supply chain disruptions and higher maritime transport costs are affecting trade flows and potentially port activity at the regional logistics hub of Lomé.

- Zambia: The landlocked economy is exposed to the Middle East shock through its reliance on imported fuel, much of which transits via the Strait of Hormuz, leading to sharply higher import costs and supply risks, with a state of crisis declared in April 2026. While higher copper prices offer some support, rising energy and input costs, including sulphur, are squeezing mining margins, limiting the net benefit. At the same time, ongoing drought conditions and the expected El Niño are amplifying inflationary pressures through reduced agricultural output.