A couple weeks ago, Steve Eisman, who predicted the subprime mess (Steve Carrell played him in The Big Short), interviewed me, and asked me how the AI boom might all fall apart.

For reasons I am about to explain, that interview, recorded May 22, now seems supremely relevant.

Here are two snippets. (Some parts of Snippet 1 are currently paywalled in a separate video but may come out soon for free; I will update with a link if they do.)

After that, I will explain why all this seems super relevant today.

Eisman: Assuming it’s a bubble. I mean if it’s not if if we’re wrong and it’s then and it’s not a bubble and and … they’ll they’ll be able to charge for the tokens and it’ll all become profitable and it’ll be and that’ll be clear within a year or so, then …

Marcus: Yeah. I mean I like to think of [the giant GenAI investments[ as it’s a bet. I think it’s a low probability of the bet coming through, but it’s not zero. It’s not

Eisman: Zero. But if it’s going to break, like in, you know, what what broke Subprime? What broke Subprime was the credit quality got so bad that the end user, the investor, stopped buying the paper. And that was the end. Because if the end user, the investor stopped buying the paper, the whole machine stopped dead in its tracks. The question I ask for you is: I mean, I wonder if maybe what will break it if it breaks is that the industry moves to this token pricing and people say, Screw you. I don’t wanna I don’t I don’t wanna pay.

Marcus: So that could certainly happen.

Eisman: And if or and if maybe that what what else do you think could happen?

Marcus: Well, so in a version of yours, and then I’ll give one of my own, what think might happen is that at some point one of these companies can’t really afford to keep losing money. Right? They’ll run out of VC money, they tap the public markets as much as they can.

My best candidate for this is open AI. Open AI, I think, has a problem right now. They are burning money the fastest. Okay.

Eisman: Which is what?

Marcus: They do not have the deep pockets that Google does. Right. They had a lead but they squandered it.

Eisman: Google got caught up and passed them.

Marcus: And then Anthropic did. I mean, maybe now they’re all kind of in a tie, but think about it compared to a few years ago. You know, everybody thought (not me, but almost everybody) thought that OpenAI was amazing. Sam Altman could do no wrong. Right. Now nobody trusts Sam Altman, there was the New Yorker story, there was the testimony in the Elon Musk trial. It’s pretty clear he should not be trusted. So I’m a company thinking you know, hypothetically, thinking about buying these services.And my choices are OpenAI, Anthropic, Google, maybe Amazon. I might not go to OpenAI anymore. And you know, th that’s reflected in the choices people are actually making, right? Anthropic has taken a lot of the business market and OpenAI has lost a lot of it. Google is fighting hard for that. So there’s a scenario. I tend to think that OpenAI is the one that goes down first. They’re also spending most money with least assets. they’ve made the most commitments. At some point they might not be able to pay their bills. Now, what they have done is they’ve kept raising the valuation. They’re starting, as your listeners might actually understand, to do weird things on preferred shares and contingencies on that funding, like some of the Amazon funding is contingent either on achieving AGI or IPOing, et cetera, et cetera. So they’re they’re making more and more concessions to the investors. They’re I saw one report that they’re offering private equity sa guaranteed seventeen point five percent returns. Which reminds me of Madoff and, you know. somebody else said maybe that’s like a first in kind of money thing, but there’s something that Reuters reported around this. You know, none of the paper is public, so we don’t know exactly. But you know, it’s pretty clear that they’re making more and more concessions to investors. They’re more and more urgent. I mean, the the biggest news just in the last few hours is that they want to rush their IPO in front of Anthropic…. they’re clearly afraid of anthropic. I think you will [see] when the numbers are really fully out, then anthropic is more efficient. we don’t know exactly why that is, but they’re more efficient. they’re less leveraged out to the hilt. They’ve made fewer promises. And so if I had the prospectuses of the two, you know, independent of what I think about the companies anyway, I’m pretty sure if I was had to invest in one, I would do Anthropic and not OpenAI. And so at some point, I think OpenAI is gonna have a problem where they can’t really meet their obligations.

And if they do, that’s gonna have ripples throughout the market. And it’s gonna be interesting sets of ripples. So

Eisman: Ripples … it’s gonna be [a] frickin’ tidal wave. I mean, as an example, Oracle, and full disclosure, I own a little bit of Oracle. I sometimes I lose sleep over the fact that I own Oracle. When Oracle reported its third quarter numbers, the stock was like 230 before they reported. And they reported these big numbers and then they came out with I can’t remember what the word was, but it is is like a version of backlog.And the backlog was like five hundred and fifty billion and it was up like eighty five percent and everybody went absolutely insane. And the stock went from like two hundred and thirty to three hundred and thirty. Like like overnight. Well

Marcus: I wrote about that on September eleventh [2025], I know exactly when it was.I wrote a piece that I called Peak Bubble. Right. And my claim was not that Oracle would never go higher than that, but that we would look back on that moment which you’re now talking about as that kind of height of absurdity of all of that. Well the prob…

Eisman: [the] problem was it turned out, you know, two days later everybody figured out that of the five hundred and fifty billion [projected revenue], like three hundred and fifty billion was just [from] openAI. That’s right. Everybody said, wait a second, I’m now completely dependent if I own Oracle, I’m now completely dependent on V C raising money for open AI to fulfill its obligations to Oracle. And the stock went from three thirty to one hundred eighty.

Marcus: Right And [Oracle] has kind of hovered around there. Maybe it’s two hundred now or something. But it basically dropped within a few days or a few weeks of I think it took a few weeks. Right. But within a few weeks it had had dropped down. And so it was at like 310 when I wrote my article Peak Bubble.

Eisman: So if you’re telling me that openAI is a problem, the ripple effects are big. I mean, this is not like, you know, some little subprime mortgage company. I mean, this is a massive company with massive obligations to massive tech companies whose names we all know. Right.

And the ripple effects would be … are going to be huge.

Marcus: That’s right.

So that is my, you know, most likely scenario. There are others, but that that is the most likely scenario to me is that openAI at some point can’t really make ends meet. Anthropic eats their lunch, Google eats their lunch, people have less confidence in them, et cetera. Right. And then you have all this stuff booked for Oracle, for NVIDIA.

….

Eisman: Yeah.

Marcus: You know, and I frequently use the metaphor of Wily Coyote over the edge of the cliff

Eisman: where he’s kinda like flailing his legs and doesn’t fall.

Marcus: Yeah. And then he looks down and he falls. That could be the moment where everybody’s just like, Okay, we’ve got this wrong.

We also talked about token economics:

Marcus: So agents are basically systems that will do things on your behalf. So they might make travel plans for you, or they might run code for you, they might write code for you. So we had this paradigm initially with ChatGPT, and it actually goes back to before ChatGPT, but where you would type in a question and you get an answer. And it might be like a yes or no query or, you know, tell me where you know where William Shakespeare was born.

The agent paradigm is different. You basically say, do stuff for me.

And the reason that those tend to be more expensive is that they tend (with the help of some good old fashioned AI that nobody wants to talk about) to run multiple large language models in the background many times until they get the answers that by some criteria seem to correct. And so sometimes they end up taking, you know, a thousand times more computational or compute or or a million times or billion times or whatever. And so the prices of the agents have been quite high.

Eisman: So let’s talk about the economics of this, because what I’ve read is there’s a there’s a cost for the tokens, and any service that anybody has signed up for, which is the a subscrip most b basically a subscription model, is way lower than the actual cost to create the answers that that we know why did Julius Caesar cross the Rubicon and it’s certainly a hell of a lot less than any agent. So now the industry is starting to shift to token pricing. I think Microsoft is about to launch it any day now. And my question for you is this is going to be a lot more expensive. And how are people going to react to this? I can’t I can’t imagine positively.

Marcus: It’s a question of who assumes the cost. So maybe a metaphor here is an all-you-can-eat buffet. You know, these these companies were serving all-you-can-eat buffets and people were eating a lot, especially when they started using agents. And the margins here are either very slim or negative in many cases, meaning that it’s costing the companies more to serve the tokens than than than you’re paying them to use it. And so they’re in a bind and it’s especially kind of pointed or poignant bind because these companies want IPO. And so they’re trying to, you know, make their numbers lookgood in some way. And it’s this trade-off because basically they’ve been running this stuff at a loss. And with the agents come along, it’s an even bigger loss. And so they’re like, you know, on the one hand, they want to get customers to use their stuff, and they’ve beenpretty effective at that. But on the other hand, they want to make a profit. And those are actually kind of in tension, right?

They’re always in tension to some extent, right? You know, the the smaller your margins, the more your customers like it. but it is turning out that it is a little bit like an all-you-can-eat buffet. And some customers were not eating that much. But when people started using things like OpenClaw, which is a kind of system for using LLMs as agents, some people started eating an awful lot at the buffet

The question is, how do you make this economically viable?

First of all, domino one: tokenmaxxing has indeed clearly died, just as Eisman and I had anticipated a few weeks ago. The LLM providers no longer want to offer all-you-can-eat and customers no longer want to pay for a la carte. The fundamental problem is that to make a reliable version of the product you either have to charge more than customers want to pay, or the providers have to take a loss. Then again, if you read this newsletter regularly you already knew that. (Others perhaps learned it today; confirming what I had been saying for weeks, ZeroHedge just reported that Citrini Research “ has written a follow up on the status quo of the AI ecosystem, noting that in just weeks we’ve gone from tokenmaxxing to tokenpanic.”)

The death of tokenmaxxing means less revenue for the LLM companies, which can only hurt the IPOs. And more and more people are noticing.

But, domino 2, something else just broke. And it may be deeply important.

It needs some context.

The context is that around a month ago SoftBank tried to take a $10 billion margin loan based on its (very large) stake in OpenAI. This didn’t go over well with the banks, as Bloomberg noted (and I as mentioned in earlier essay):

Kalani o Māui@MauiBoyMacro

5:20 PM · May 8, 2026 · 460 Views

3 Reposts · 7 Likes

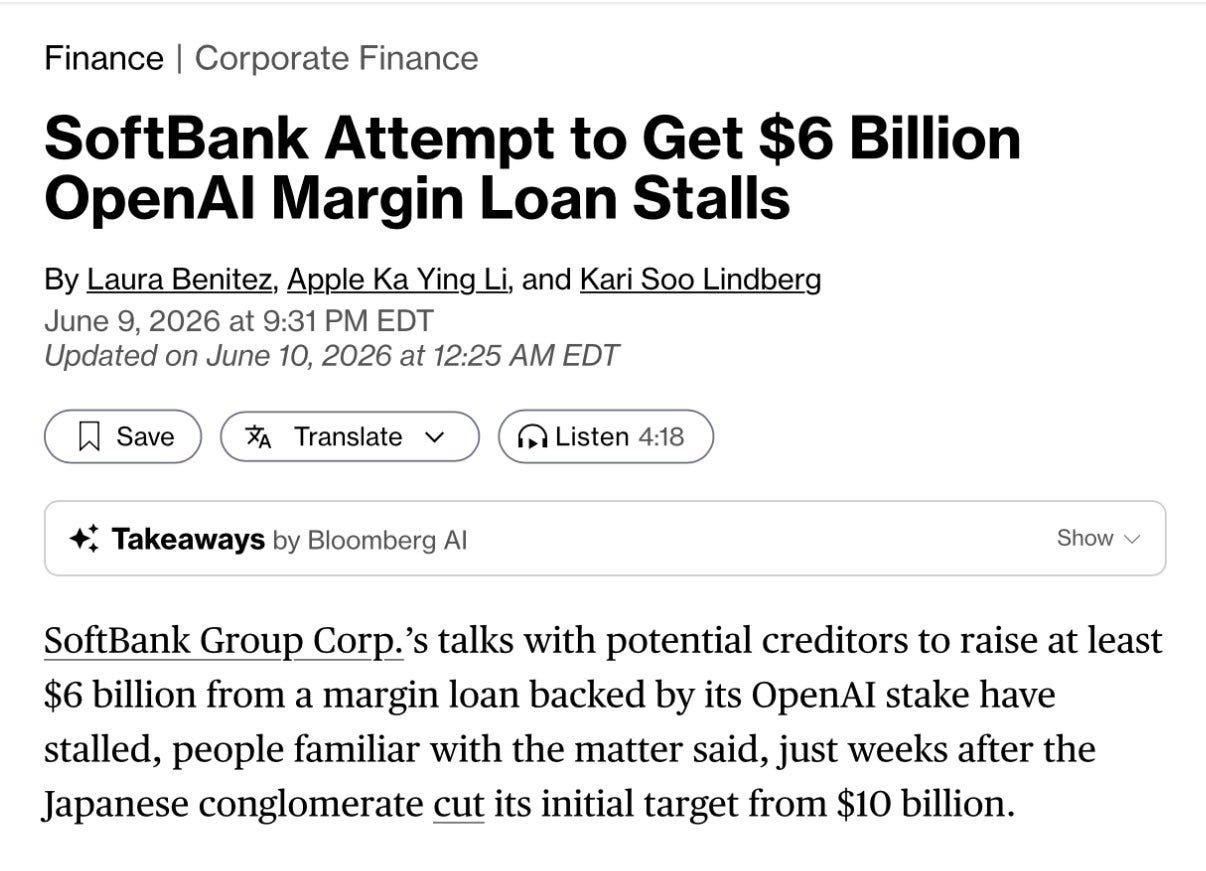

The new, breaking news is even worse. Bloomberg is now reporting that the banks don’t even want to do the smaller loan:

SoftBank took an immediate hit; dropping the ask reeks of desperation, and its a terrible vote of nonconfidence that the banks still said no:

Financelot@FinanceLancelot

BREAKING: SoftBank shares fall 9% after its attempt secure a $6 billion margin loan backed by its stake in OpenAI fails.

6:28 AM · Jun 10, 2026 · 52.5K Views

47 Replies · 110 Reposts · 577 Likes

That’s domino 2: we can infer that the banks don’t really think that OpenAI is worth its current valuation. They don’t want OpenAI stock as collateral.

And OpenAI wants to IPO at even higher valuation. That’s going to be hard given this news.

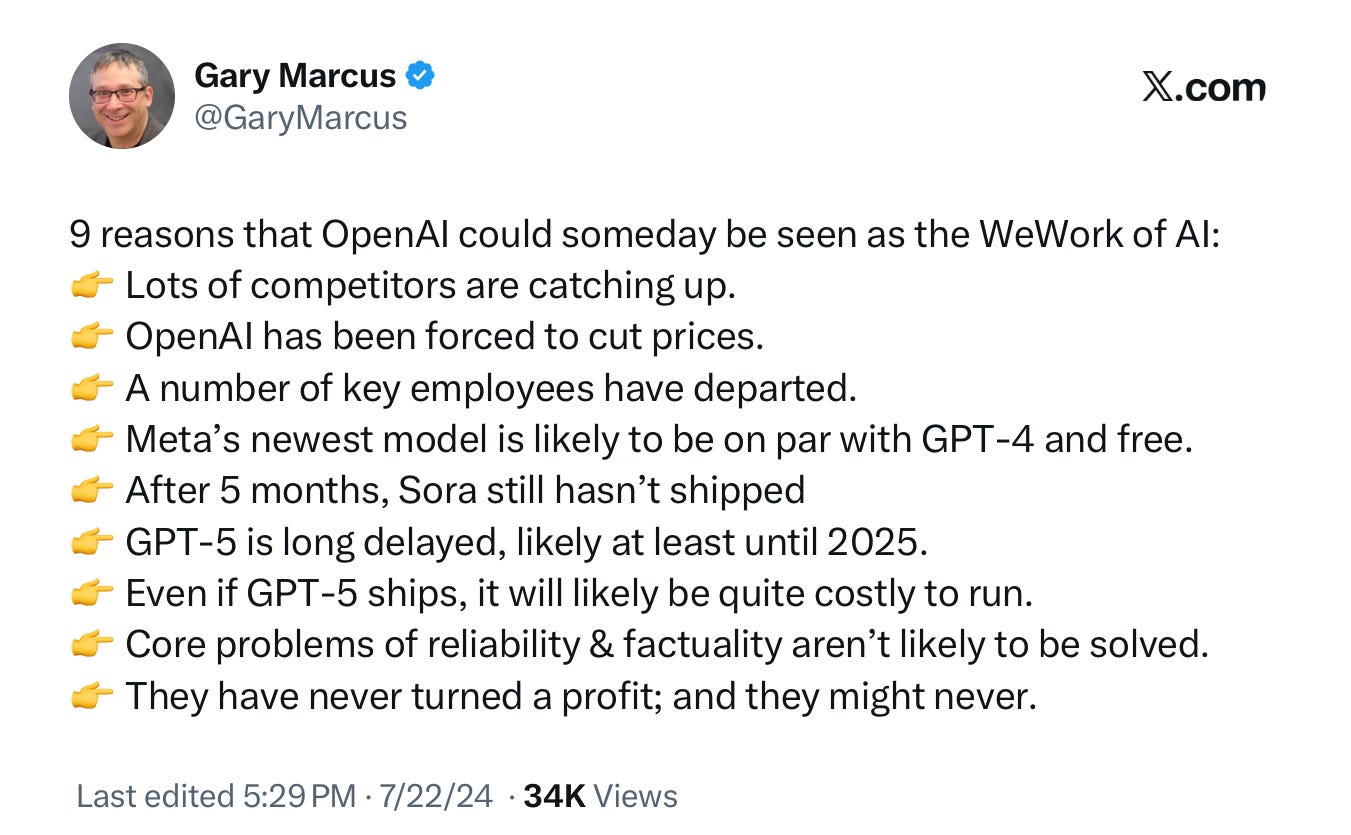

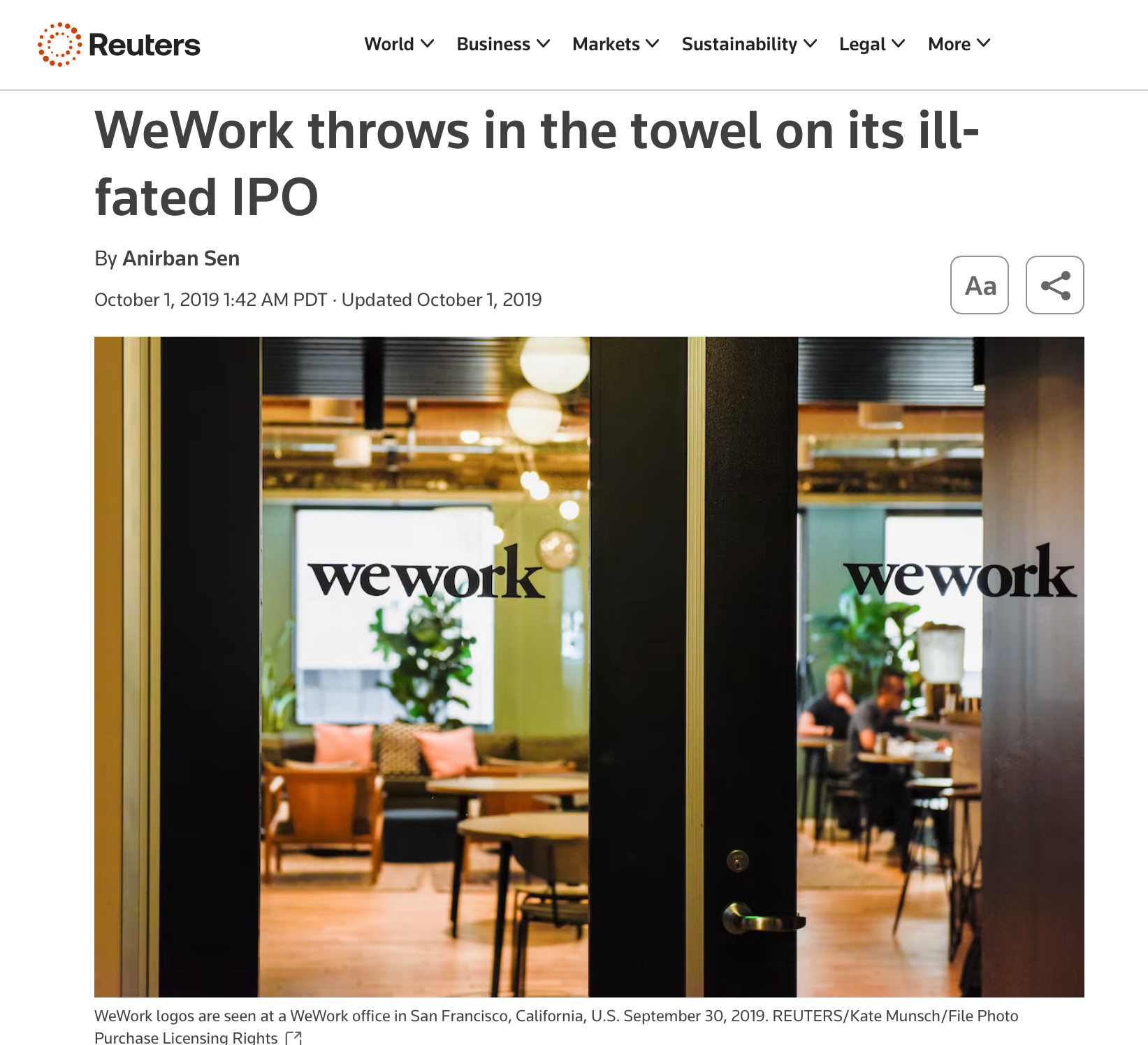

So maybe domino 3 is this: OpenAI may well wind up as the WeWork of AI. (Trivia fact: Masa famously invested big in WeWork just before they fell).

Here’s a version of the argument I made two years ago:

Two years later, competitors have caught up. OpenAI has had to cut prices. More key employees left, Opensource models (though perhaps not Meta’s) are only a few months behind. Sora briefly shipped but ultimately was pulled from the market altogether. GPT was delayed (until August 2025, as predicted). The latest models (though not 5 specifically) are costly to run, and cost is a growing issue. Core problems of reliability and factuality haven’t been solved,. And OpenAI still has yet to turn a profit, and it’s still not clear they ever will.

Every bad sign is worse now. The big difference is that people are finally noticing.

For perspective, my tweet above got a measly 34,000 views; now the entire world is worried about whether AI is a bubble. And rightly so.

That Wile E Coyote moment could turn out to be soon.

Which takes me directly to Part III.

What happened, of course with WeWork is that they were planning an immense IPO, and everything fall apart; in October 2019, not long after raising an enormous round from Softbank, they withdrew their IPO.

If the market gets squirrelly on OpenAI’s IPO, which after today seems like a real possibility, OpenAI might be forced to withdraw its IPO (Domino 3), or to cut their aspirations sharply. If so, I don’t see how they could meet their immense ($600 B) obligations. (Domino 4)

If they can’t meet their obligations, I expect Nvidia and Oracle and many others would take a big hit as collateral damage (Domino 5). And the damage might affect the banking system, retirement plans and more (too many dominoes to count). There would definitely be discussions of bailouts.

(Disclaimer: This is not investment advice, it just what I am seeing. Use these thoughts at your own risk.)