On April 1st, the European Commission proposed to modify the functioning of the Market Stability Reserve (MSR), so that the allowances held in the reserve are not invalidated. Just a year ago, such a proposal would have sounded like an April Fool’s joke, but it actually happened.

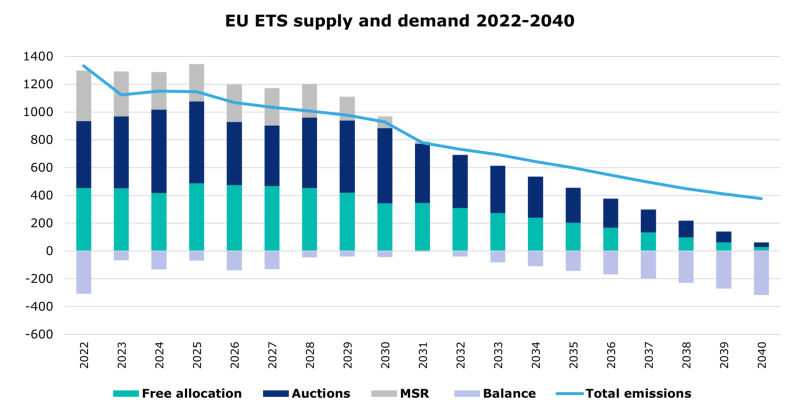

In a perfect world, the energy sector and industry would decarbonise at the same pace as the shrinking number of total cap of allowances. European leaders hoped that this would materialise and both sectors could achieve the climate neutrality around 2040. In such a scenario, the demand for emission allowances would substantially decrease and the low liquidity of EU ETS would not be an issue. But, these expectations proved wrong and in the coming years the shortage of allowances in relation to actual emissions will only grow (see graph below).

Source: PGE based on the data from the European Commission, European Environment Agency (EEA), European Energy Exchange AG (EEX).

The MSR was launched in 2019 with the aim to absorb the oversupply caused by the 2008-2010 economic crisis. Apart from that, in 2018 the emission allowances were also classified as a financial instrument, which was overlooked by the most of compliance entities. This decision led to the situation where a significant pool of allowances is held on the accounts of investment funds, that aim to benefit from selling them in the future.

These volumes are not available for other market participants, but due to the design of EU ETS, such allowances appear for the MSR as available on the market. With the shrinking number of allowances, MSR proved to be one of the main price-drivers responsible for the major decrease of supply of allowances available for the market participants: 3.2 billion of allowances in total were invalidated by the MSR by the end of 2024.

The Commission’s MSR proposal means that all allowances exceeding the 400 million threshold held in MSR will no longer be invalidated. To put in in a perspective – in 2025 ca. 270 million of allowances, worth around €19 billion (in the current prices) were invalidated. This accounts approximately to the equivalent of the allowances auctioned to finance €20 billion the RePower EU programme, which aimed to improve the resilience of the European energy infrastructure and is three times more than funds dedicated for energy infrastructure under the current CEF Energy framework. Under the current EU ETS parameters, the MSR will be empty around 2035 and unable to stabilize the market.

It is clear that a major overhaul is needed and that the EU ETS must also take into account EU’s competitiveness, resilience, and ability to react to price shocks. Figuratively speaking: we cannot just push the car anymore, it needs a new engine. So, what should come next to prepare the EU ETS for the future challenges?

Firstly, EU ETS must aim not only at the emissions reductions but at energy security and affordability of prices. The gas-fired power plants will be important to stabilize energy systems in the countries like Germany or Poland, and such plants will influence energy prices and also be important for the district heating systems. At the same time, the rising EU ETS prices and their volatility will impact the operating costs of such installations and power prices around the Europe.

According to Draghi’s report on EU competitiveness, the carbon cost accounted for around 10% of the EU industrial retail electricity price in 2023. Also the European Council’s conclusions from 19 March called on the EC “to reduce the volatility of the carbon price and mitigate its impact on electricity prices”. This is a well-desired relief for the European economy. It is worth mentioning that only in Poland does the carbon cost account for 50% of energy price paid by industrial users.

Therefore, at least peaking units, most needed for the stabilisation of the power systems, should be exempted from the obligation to surrender allowances. This will have a little effect on the total emissions with an important impact on the power prices.

EU ETS also severely impacts district heating which serves ca. 70 million of Europeans. To make heat prices more affordable and ease the transformation of this sector, the free allocation of allowances should be continued, including allocation for investments. Furthermore, the realistic benchmark methodology should be set to reflect a more accurate pace of emissions reduction for this sector.

In the long-run, electricity will be fully decarbonised, thus not bearing the carbon cost anymore. However, further decarbonisation of power systems becomes more challenging – remaining emissions are more costly and difficult to abate. Since the whole economy benefits from the energy infrastructure, the initiatives, like recently announced €30 billion ETS Investment Booster, should support energy sector too. It is also of the utmost importance to maintain in the post-2030 framework the Modernisation Fund, which needs to be continued and increased.

Secondly, ensuring market liquidity. The already mentioned abolition of invalidation by the MSR is the right move, but more needs to be done. For instance, lowering of the Linear Reduction Factor (LRF) to reach climate neutrality by 2050 (not 2040 as it is right now) or integration of the international carbon credits with the EU ETS. As result, the overall pool of allowances would not shrink so rapidly allowing further decarbonisation in the industrial sectors, which will require more effort and time.

Thirdly, the resilience to shocks. The EU ETS lacks any effective measure to prevent price shocks. The current mechanism under Article 29a of the EU ETS Directive has never been activated. The MSR does not react to prices, but the supply levels. However, it reacts with more than 1 year lag and the decision is based on data that does not reflect market realities. As it was mentioned before – the Total Number of Allowances in Circulation (TNAC) indicator, which activates the MSR, also includes the allowances that are held on the accounts of the financial institutions to generate revenues in the future – so they are not available for the market participants. Therefore, the MSR should be activated on the basis of reaching specific price levels, not virtual TNAC.

As the EU ETS market will shrink, we should pay more attention to behavior that might fuel the excessive speculation, which is depicted by the latest market developments (see graph below). Despite a harsh winter and growing demand for electricity, including conventional units, the carbon price dropped significantly due to the political discussions on the EU ETS. Therefore, market oversight should prevent excessive speculation by introducing position limits for non-compliance participants.

Source: PGE based on the data from the European Energy Exchange AG (EEX).

These three areas require urgent action. The EU ETS is a pillar of EU’s decarbonisation efforts, so the reforms will not be easy, but they are necessary to make the climate policies not only ambitious but credible as well. We cannot afford to kick the can down the road any longer. It is important to adjust the EU ETS to confront current challenges in a way that will ensure the competitiveness of European industry. The upcoming reform is a big, and perhaps last, chance for that.

Marcin Laskowski is Vice-President of the Management Board for Regulations at PGE.