India is in a position of greater resilience than in earlier crises.

The Middle East conflict is sending shockwaves through the global economy. Markets are grappling with two major unknowns: how long the conflict will last and how high it could push energy prices if disruption persists.

For India, rising oil prices have historically left the country exposed because of its reliance on imported energy. But things are different this time around.

Structural shifts have made India more resilient to external shocks and recent market weakness has pushed valuations in a growing number of high-quality, domestically focused businesses back to attractive levels.

For investors, this is an area worth monitoring closely.

Reduced oil price sensitivity

One of the clearest channels through which the conflict is affecting markets is the oil price. The closure of the Strait of Hormuz, through which roughly a fifth of global oil supply normally passes, has intensified concerns around supply disruption. Oil has already moved above $100 a barrel and remains around that level today.

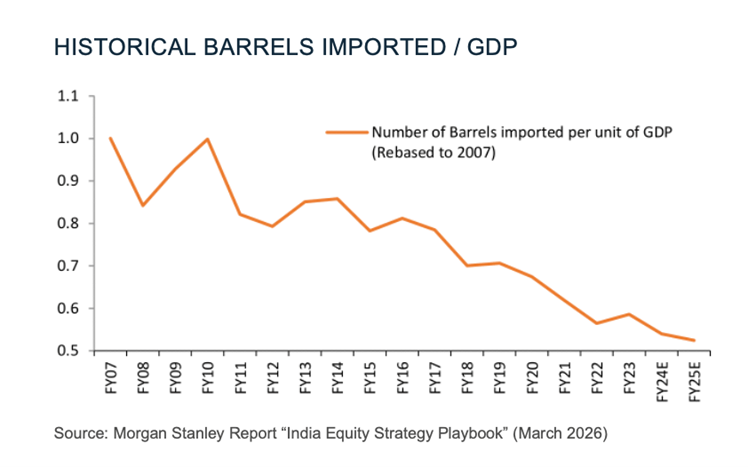

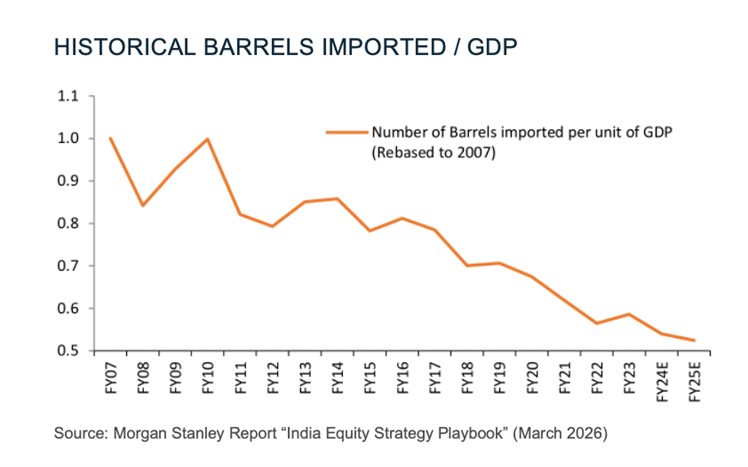

That would once have been a much more serious macro threat to India. Previous energy price spikes, such as the one in 2013, exposed how vulnerable the country was to higher import costs. However, the structure of the economy has changed materially since then.

India’s GDP has more than doubled since 2013, yet its oil import bill in dollar terms has risen only modestly. The country’s import basket has diversified; electronics, gold and machinery now account for a larger share, while petroleum has fallen from 37% to 26% of total imports between 2014 and 2025.

As the below shows, barrels imported per unit of GDP have been falling steadily for some time now.

Source: Chikara

That shift is being reinforced by the rise of renewables – from a 23% percentage share of capex in 2014 to more than 40% in 2025 – and by services, the least oil-intensive part of the economy, driving a growing share of GDP growth.

None of this means oil no longer matters, of course, but it may indicate that India is less sensitive to an energy shock than in previous crises.

Resilient domestic economy

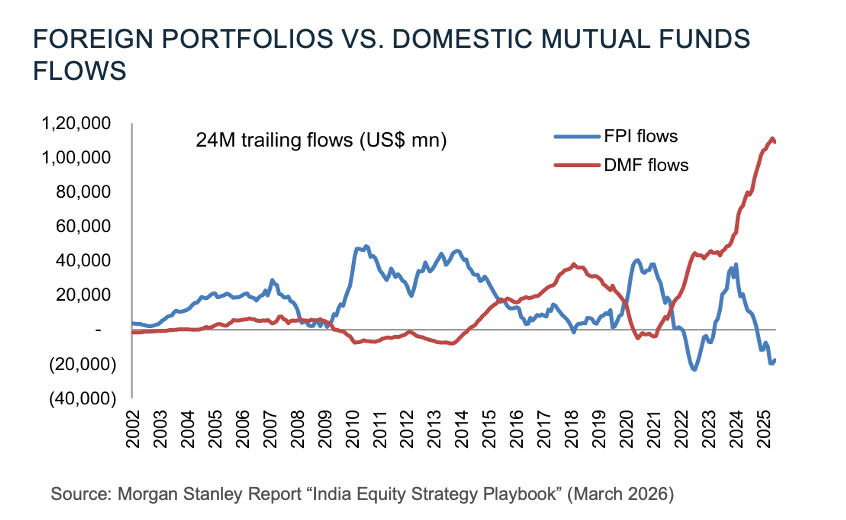

Another major consequence of the conflict for India, as in most economies, has been foreign portfolio outflows. These now total around $12bn year-to-date, exacerbating a trend seen since 2022. That marks a sharp contrast with the prior decade, when India attracted consistent net foreign inflows.

What’s different this time is that the domestic economy has become a much stronger buffer. GDP has more than doubled since 2013, with around 60% of growth now driven by domestic consumption. That gives India a deeper, powerful internal engine of demand when global conditions turn uncertain.

Policy has supported that resilience. Recent income tax cuts and a significant reduction in Goods and Services Tax – introduced last year to blunt the impact of US tariffs – have helped underpin household confidence and spending.

Wealthier Indian households are also saving more through financial assets. As the chart below shows, domestic mutual fund inflows have risen sharply in recent years to the point where they are now effectively absorbed foreign selling.

Source: Chikara

That marks an important structural change. Foreign outflows still affect sentiment but they no longer have the same overwhelming power to dictate the direction of the Indian market.

Covid-level valuations

Taken together, reduced oil sensitivity and a resilient domestic economy leave India better placed to absorb an external shock like the Iran conflict than in the past.

And that’s an important backdrop to remember right now, because immediate market weakness is creating a very interesting valuation backdrop; valuations across the market have fallen back to levels not seen since the Covid period.

That creates an opportunity for long-term investors willing to look through the near-term noise. Companies with net cash balance sheets and strong pricing power may continue to gain market share in more volatile environments over time, yet they are currently trading well below their long-term median valuations.

Those willing to wait out the disruption may benefit from a re-rating once conditions begin to normalise.

Long-term opportunity

The immediate backdrop is uncertain. Higher oil prices, geopolitical tension and foreign outflows are all valid reasons for caution. But India enters this period from a position of greater resilience than in earlier crises.

Its economy is less exposed to oil, more supported by domestic demand and increasingly underpinned by domestic savings flows that can absorb bouts of foreign selling.

That suggests recent drawdowns may be creating a more attractive entry point into durable, high-quality businesses with strong domestic growth runways.

For long-term investors, this period may look less like a warning sign and more like a shift towards more reasonable valuation levels.

Andy Draycott is portfolio manager of the Chikara Indian Subcontinent fund. The views expressed above should not be taken as investment advice.