Shift in Indian styrene trade flows

The strait of Hormuz disruption has significantly altered styrene trade, especially for India. These changes can be understood across three main areas: supply disruption, trade rerouting, and shifts in market power.

Before the war, India depended heavily on the Middle East region for styrene imports. Short shipping distances, readily available feedstocks, and low freight costs made the region a reliable and low-cost supplier for India.

Supply disruption

The US/Iran war caused styrene exports from the Middle East to fall sharply. Major producers like SABIC and Equate declared force majeure. At the same time, shortages of key feedstocks reduced styrene production globally, tightening global supply.

Supply shortages and transport issues pushed styrene prices higher. This created both a supply shock and cost pressure across the styrenics sector.

Trade rerouting

With less supply from the Gulf, India turned to Northeast Asia. Key suppliers now include China, and Taiwan.

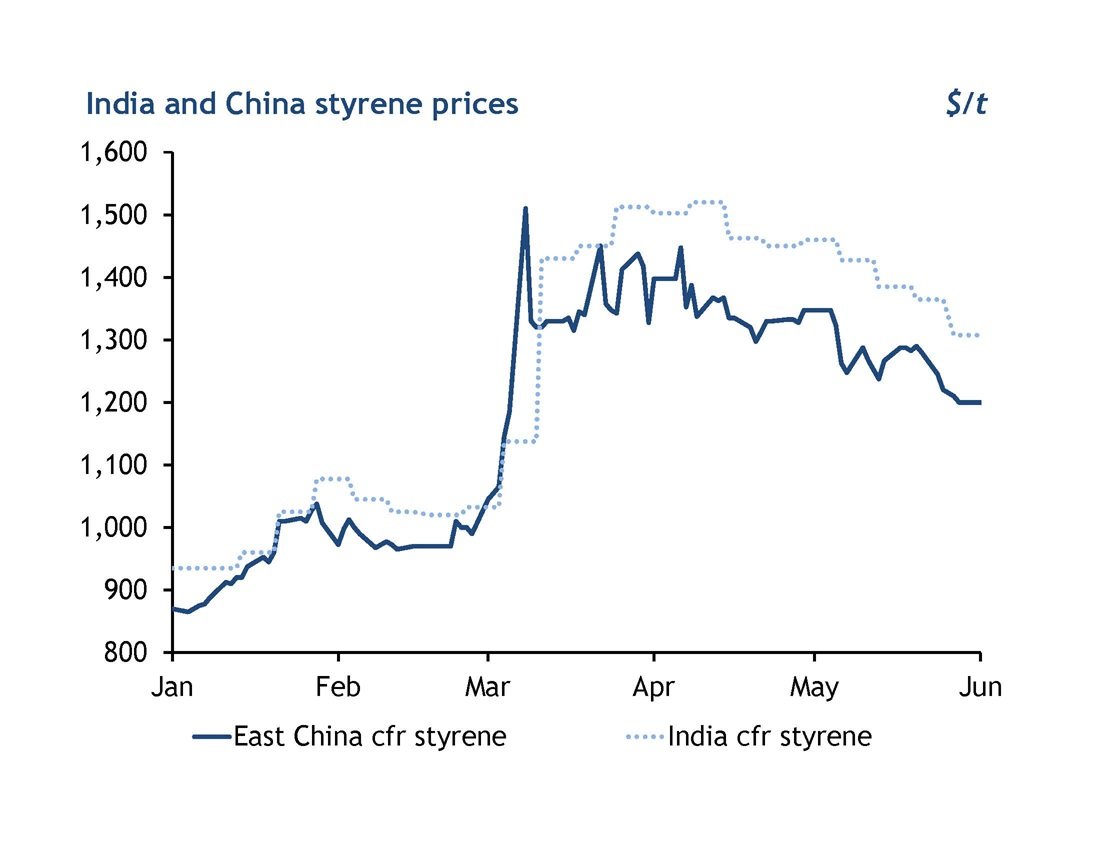

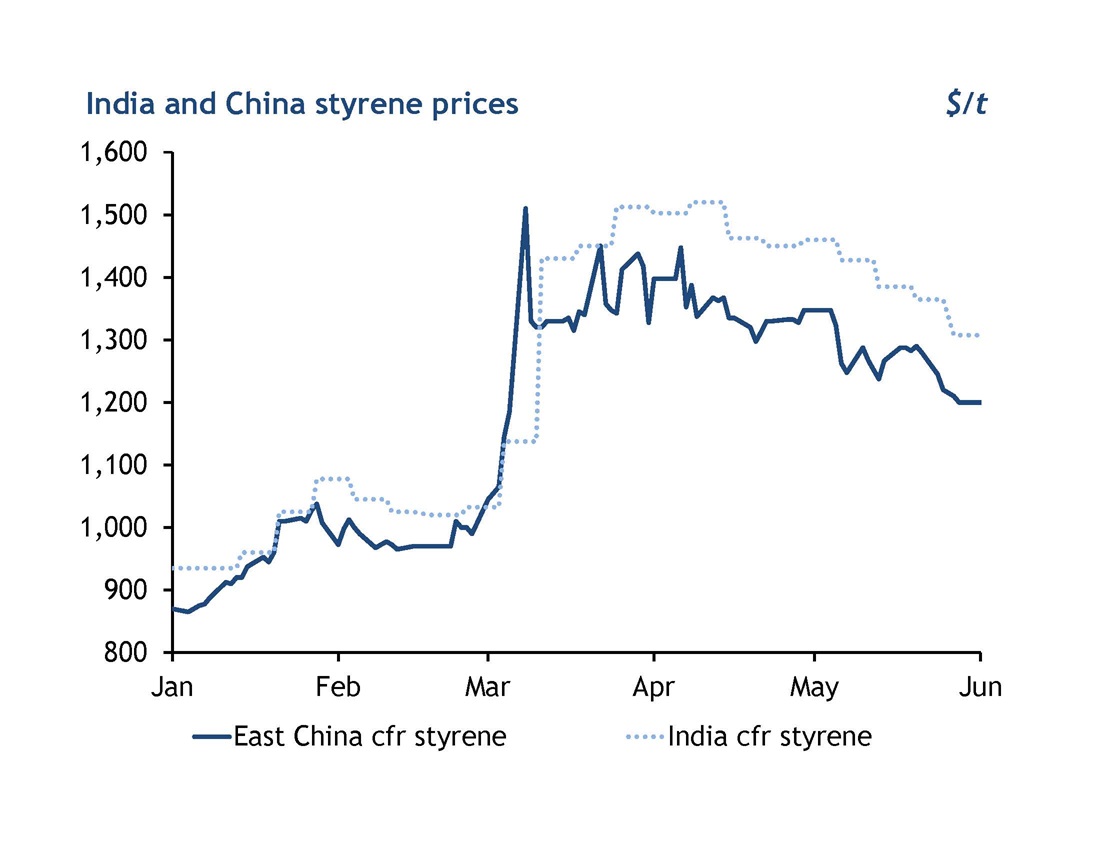

This shift has drawbacks: shipping takes longer and costs more. Indian buyers had to pay a premium for these cargoes when they switched suppliers. This is illustrated in the first chart, which shows the divergence between Chinese and Indian styrene prices. China is thus leveraging the disruption in the Middle East to expand its market share in India. Chinese producers have faced weaker domestic demand, especially from the construction and consumer goods sectors. This has led to increased pressure to clear the existing volumes.

A key question remains whether Chinese suppliers will seek to retain and defend this share over the longer term, or if Middle East producers will be able to reclaim lost volumes once supply conditions stabilize. At the moment, it is unclear whether the shift is temporary or permanent. Middle East suppliers still have strong advantages, including geographic proximity, established trade relationships, and integration with feedstock sources. When their production is stable and pricing is competitive, they are likely to regain share.

Buyers have shifted their strategy in response to new trade patterns. Previously, they held one to two months of inventory. Now, they maintain only a few weeks of stock, allowing them to better manage risk in uncertain conditions.

Meanwhile, Asian suppliers face limits. Feedstock shortages and lower run rates limit supply and increase competition for available cargo.

-Argus data

-Kpler data

Market shifts

India now depends more on distant suppliers and faces higher costs for styrene. At the same time, Chinese suppliers have gained market share at the expense of traditional exporters.

The crisis is likely to push India to diversify supply sources and reignite a push for domestic styrene capacity.